Current Affairs

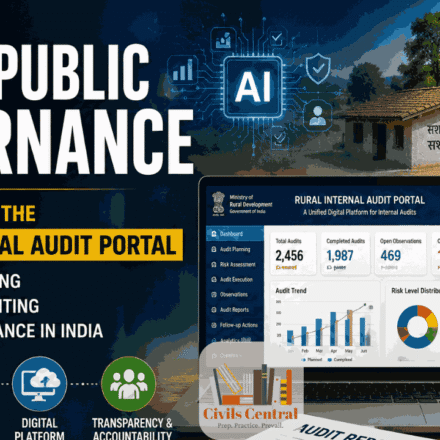

On 28 June 2026, Union Minister for Rural Development Shri Shivraj Singh Chouhan launched the AI-enabled Rural Internal Audit Portal during the Rashtriya Gramin Vikas Sammelan held at Pusa Campus, New Delhi. The portal has been described as India’s first unified digital platform for end-to-end management of internal audits covering both compliance audits and risk-based audits within the Ministry of Rural Development.

While the announcement concerns a new digital platform, the larger UPSC themes extend far beyond the portal itself. The development brings together several important concepts such as good governance, transparency, accountability, artificial intelligence, internal auditing, public financial management, digital governance, rural development, and technology-driven administration.

Introduction

Governments throughout history have sought to answer a fundamental question: How can public resources be managed honestly, efficiently, and for the benefit of citizens? As societies became more complex, governments expanded their responsibilities to include education, healthcare, infrastructure, social protection, agriculture, environmental conservation, and economic development. With increasing public expenditure came the equally important responsibility of ensuring that public money was used efficiently, legally, and transparently.

Traditional administrative systems relied heavily on manual record-keeping, periodic inspections, and post-facto audits. Although these mechanisms played an important role in maintaining accountability, they were often time-consuming, fragmented, and reactive. Irregularities were frequently detected only after significant financial losses had occurred, making corrective action difficult and reducing public confidence in government institutions.

The rapid advancement of digital technologies has transformed this landscape. Governments around the world are increasingly adopting digital platforms, data analytics, artificial intelligence, cloud computing, and real-time monitoring systems to strengthen governance. These technologies enable public authorities to detect risks earlier, automate routine processes, improve service delivery, and make evidence-based policy decisions.

India’s governance ecosystem has undergone a similar transformation over the past decade. Initiatives such as Digital India, Direct Benefit Transfer (DBT), Government e-Marketplace (GeM), Public Financial Management System (PFMS), Digital Public Infrastructure (DPI), and Aadhaar-enabled service delivery have demonstrated how technology can improve efficiency while reducing leakages and corruption. The launch of the AI-enabled Rural Internal Audit Portal represents another milestone in this journey by applying advanced technologies to public auditing and financial oversight.

However, to appreciate the significance of this initiative, it is necessary to understand the broader concepts of governance, good governance, digital governance, and the evolving role of technology in public administration.

Understanding Governance

The term governance refers to the processes, institutions, mechanisms, and relationships through which decisions are made, implemented, monitored, and evaluated within a society. It encompasses not only the activities of governments but also the interactions among public institutions, private organisations, civil society, and citizens.

Governance is therefore broader than the concept of government. While government refers to formal institutions exercising political authority, governance includes the entire framework through which public affairs are managed and collective decisions are translated into action.

In a democratic country such as India, governance involves multiple stakeholders, including:

- Parliament and State Legislatures.

- The Executive.

- The Judiciary.

- Constitutional Bodies.

- Statutory Institutions.

- Local Self-Governments.

- Civil Society Organisations.

- Private Sector.

- Citizens.

Effective governance requires coordination among these institutions to achieve public objectives while respecting constitutional values.

Government and Governance

The terms government and governance are often used interchangeably, but they represent distinct concepts.

| Government | Governance |

|---|---|

| Refers to formal political institutions exercising authority. | Refers to the overall process of decision-making and implementation involving multiple stakeholders. |

| Primarily involves elected representatives and public officials. | Includes government, civil society, private sector, and citizens. |

| Focuses on exercising authority. | Focuses on how authority is exercised effectively, transparently, and accountably. |

| Institutional concept. | Process-oriented concept. |

Thus, governance is concerned not merely with who governs but how governance is conducted.

Evolution of Governance

The concept of governance has evolved significantly over time.

Traditional Administration

Historically, public administration was characterised by:

- Centralised decision-making.

- Rigid bureaucratic procedures.

- Paper-based records.

- Limited citizen participation.

- Hierarchical control.

Success was often measured by adherence to rules rather than outcomes. Although this system ensured administrative order, it frequently resulted in delays, inefficiency, and limited responsiveness to citizens’ needs.

New Public Management

During the late twentieth century, many countries introduced reforms inspired by the principles of New Public Management (NPM). These reforms emphasised:

- Efficiency.

- Performance measurement.

- Decentralisation.

- Customer orientation.

- Results-based management.

- Financial accountability.

Governments increasingly adopted management practices traditionally associated with the private sector while maintaining public accountability.

Digital Governance

The rapid expansion of information technology transformed governance further. Governments began using digital platforms to:

- Deliver services electronically.

- Improve transparency.

- Reduce administrative delays.

- Enhance accessibility.

- Improve record management.

Digital governance represented a shift from paper-based administration towards integrated electronic systems.

Intelligent Governance

The emergence of Artificial Intelligence, Big Data, Machine Learning, Blockchain, and predictive analytics has introduced a new stage in governance. Instead of merely digitising existing processes, governments now seek to make governance:

- Predictive.

- Data-driven.

- Intelligent.

- Proactive.

- Personalised.

- Evidence-based.

The Rural Internal Audit Portal exemplifies this transition by applying AI to audit planning, risk assessment, compliance monitoring, and financial oversight.

What is Good Governance?

The concept of Good Governance gained global prominence during the 1990s through organisations such as the World Bank, the United Nations Development Programme (UNDP), and the Organisation for Economic Co-operation and Development (OECD).

Good governance refers to the manner in which public institutions conduct public affairs, manage public resources, and guarantee the realisation of human rights while ensuring efficiency, accountability, transparency, participation, and the rule of law. It is not simply about administrative efficiency; it is about governing in a manner that serves citizens fairly, responsibly, and effectively.

Characteristics of Good Governance

Although different institutions use slightly different frameworks, good governance generally incorporates the following principles.

Participation

Citizens should have meaningful opportunities to participate in public decision-making through elections, consultations, local self-government institutions, and public engagement. Participation strengthens democratic legitimacy and improves policy outcomes.

Rule of Law

Governance must operate within the framework of constitutional and legal principles. All individuals and institutions, including the government itself, are subject to the law. The rule of law prevents arbitrary exercise of power and protects citizens’ rights.

Transparency

Government decisions, policies, procedures, and expenditure should be open and accessible. Transparency reduces opportunities for corruption while increasing public confidence in institutions. Digital platforms increasingly strengthen transparency by making information publicly available in real time.

Accountability

Public officials must remain answerable for their decisions and actions. Accountability mechanisms include:

- Internal audits.

- External audits.

- Parliamentary oversight.

- Judicial review.

- Social audits.

- Citizen feedback.

- Performance evaluation.

The Rural Internal Audit Portal directly strengthens this pillar by improving internal accountability within government programmes.

Responsiveness

Governments should respond promptly and effectively to citizens’ needs. Technology enables faster grievance redressal, improved communication, and real-time service delivery.

Effectiveness and Efficiency

Public resources should be utilised optimally to achieve intended developmental outcomes. Efficiency involves reducing waste, delays, duplication, and unnecessary administrative costs.

Equity and Inclusiveness

Development should benefit all sections of society, particularly vulnerable and marginalised communities. Inclusive governance promotes social justice and equal opportunities.

Consensus Orientation

Governance often requires balancing diverse interests through dialogue, consultation, and consensus-building. This promotes social harmony and sustainable policymaking.

Why Good Governance Matters?

Good governance is not merely an administrative ideal—it is the foundation of sustainable development. Efficient institutions ensure that public funds reach intended beneficiaries, welfare schemes achieve their objectives, and citizens develop trust in the state.

Conversely, weak governance can result in corruption, leakages, policy failures, delays, and inefficient use of scarce public resources. In a country like India, where large-scale programmes such as MGNREGA, PMAY-G, PMGSY, and NRLM involve substantial public expenditure, robust governance mechanisms are essential to ensure transparency, accountability, and effective service delivery.

The launch of the AI-enabled Rural Internal Audit Portal reflects this broader shift towards technology-enabled good governance. Rather than relying solely on periodic manual inspections, the government is moving towards continuous, data-driven oversight capable of identifying risks early, strengthening internal controls, and improving the overall quality of public administration.

From Good Governance to Digital Governance

The principles of good governance—transparency, accountability, efficiency, participation, responsiveness, and the rule of law—remain constant. What has changed dramatically is the method through which these principles are implemented.

Traditionally, governance depended heavily on paper records, physical files, manual verification, face-to-face interactions, and periodic inspections. While these methods established the foundation of public administration, they were often slow, resource-intensive, and vulnerable to delays, human error, duplication of work, and corruption.

The rapid development of Information and Communication Technology (ICT) has fundamentally transformed this landscape. Governments today increasingly use digital platforms, cloud computing, artificial intelligence, geospatial technologies, big data analytics, and mobile applications to improve the design, implementation, monitoring, and evaluation of public policies.

The result is the emergence of Digital Governance—a governance model that leverages technology to deliver public services more efficiently, transparently, and citizen-centrically. The launch of the AI-enabled Rural Internal Audit Portal is part of this broader transition from conventional administration to intelligent digital governance.

Understanding Digital Governance

Digital Governance refers to the strategic use of digital technologies to improve the functioning of government institutions, enhance public service delivery, strengthen accountability, and increase citizen participation.

It is much broader than simply computerising government offices. Digital Governance seeks to redesign administrative processes so that they become faster, data-driven, integrated, and outcome-oriented.

Instead of asking “How can we digitise an existing paper process?”, digital governance asks “How can technology fundamentally improve the way government functions?” Thus, digital governance represents a transformation of governance itself rather than merely a technological upgrade.

Objectives of Digital Governance

Digital governance aims to achieve several interrelated objectives.

Improve Service Delivery

Digital platforms reduce procedural delays and enable faster delivery of public services. Examples include:

- Online applications.

- Digital certificates.

- Electronic payments.

- Online grievance redressal.

- Real-time beneficiary tracking.

Increase Transparency

Digital systems automatically generate electronic records that are easier to monitor, verify, and audit. Transparency improves because:

- Transactions leave digital trails.

- Information becomes publicly accessible.

- Manual manipulation becomes more difficult.

- Decision-making can be monitored.

Strengthen Accountability

Technology enables governments to monitor implementation continuously rather than periodically. Real-time dashboards, automated alerts, and digital reporting systems improve administrative accountability at every level.

Improve Efficiency

Automation reduces repetitive manual work, minimises paperwork, and allows officials to focus on higher-value decision-making. Efficiency also improves because digital systems reduce duplication of effort and streamline administrative workflows.

Promote Evidence-Based Policymaking

Digital governance generates large volumes of high-quality administrative data. Such data help policymakers:

- Identify implementation gaps.

- Monitor programme performance.

- Allocate resources efficiently.

- Evaluate policy outcomes.

- Predict future challenges.

Enhance Citizen Participation

Digital platforms facilitate:

- Public consultations.

- Online feedback.

- Grievance redressal.

- Social accountability.

- Open government initiatives.

Technology therefore strengthens democratic governance.

e-Governance and Digital Governance

Although the two terms are often used interchangeably, they represent different stages of administrative evolution.

| e-Governance | Digital Governance |

|---|---|

| Focuses primarily on using ICT to deliver government services electronically. | Focuses on transforming governance using digital technologies. |

| Digitises existing administrative processes. | Redesigns administrative systems around digital technologies. |

| Emphasises service delivery. | Emphasises governance transformation. |

| Government-centric. | Citizen-centric and data-driven. |

| Limited integration. | Integrated digital ecosystems with real-time monitoring and analytics. |

Thus, e-Governance may be considered the first stage of digital transformation, whereas Digital Governance represents a more comprehensive and intelligent governance model.

Evolution of Digital Governance in India

India’s digital governance journey has evolved through several major phases.

Phase I: Computerisation

The earliest reforms focused on introducing computers into government offices for record management and basic administrative tasks.

Examples included:

- Computerised land records.

- Digital payroll systems.

- Electronic databases.

Although important, these initiatives largely replicated existing manual processes.

Phase II: e-Governance

The launch of the National e-Governance Plan (NeGP) accelerated the delivery of public services through digital platforms.

Government departments increasingly introduced:

- Online applications.

- Electronic certificates.

- Digital payments.

- Citizen service centres.

This phase significantly improved accessibility and convenience.

Phase III: Digital India

Launched in 2015, the Digital India Programme sought to transform India into a digitally empowered society and knowledge economy.

Its three core vision areas include:

- Digital infrastructure as a utility to every citizen.

- Governance and services on demand.

- Digital empowerment of citizens.

Digital India expanded digital governance across virtually every sector of public administration.

Phase IV: Digital Public Infrastructure (DPI)

India subsequently developed one of the world’s most advanced Digital Public Infrastructure (DPI) ecosystems.

Key components include:

- Aadhaar.

- Unified Payments Interface (UPI).

- DigiLocker.

- CoWIN.

- Account Aggregator Framework.

- Open Network for Digital Commerce (ONDC).

These interoperable platforms demonstrate how digital infrastructure can support inclusive governance at scale.

Phase V: Intelligent Governance

India is now entering the next stage of governance transformation through the integration of:

- Artificial Intelligence.

- Machine Learning.

- Big Data Analytics.

- Internet of Things.

- Cloud Computing.

- Predictive Analytics.

The AI-enabled Rural Internal Audit Portal represents one such initiative where governance moves beyond digitisation towards intelligent decision-making.

Artificial Intelligence in Public Administration

Artificial Intelligence (AI) refers to the ability of computer systems to perform tasks that normally require human intelligence.

These tasks include:

- Learning from data.

- Pattern recognition.

- Natural language processing.

- Predictive analysis.

- Decision support.

- Automation.

Unlike conventional software, AI systems improve their performance by analysing large volumes of data and identifying complex relationships that may not be immediately visible to human administrators.

Why Governments are Adopting AI

Modern governments manage enormous quantities of information relating to:

- Taxation.

- Welfare schemes.

- Healthcare.

- Agriculture.

- Infrastructure.

- Education.

- Financial management.

- Public grievances.

Manual analysis of such large datasets is increasingly impractical. Artificial Intelligence enables governments to process this information rapidly while identifying trends, risks, and anomalies. Consequently, AI supports better policymaking and more efficient administration.

Applications of AI in Governance

Artificial Intelligence is transforming multiple areas of public administration.

Fraud Detection

AI algorithms can analyse financial transactions to identify suspicious expenditure patterns. Potential frauds may be detected before significant losses occur. This is particularly relevant for public expenditure programmes involving thousands of implementing agencies.

Risk-Based Auditing

Instead of auditing every programme with equal intensity, AI helps identify projects that present higher financial or operational risks. This enables audit resources to be focused where they are most needed. The Rural Internal Audit Portal adopts precisely this approach.

Public Grievance Analysis

Governments receive millions of citizen complaints every year. AI can:

- Categorise grievances.

- Identify recurring issues.

- Detect emerging trends.

- Prioritise urgent cases.

This improves responsiveness and service delivery.

Policy Evaluation

AI enables governments to analyse programme outcomes across districts, demographic groups, and time periods. Evidence generated through AI supports more informed policymaking.

Resource Allocation

Predictive models help governments allocate financial and human resources according to projected demand rather than historical expenditure alone. This improves efficiency while reducing waste.

Disaster Management

AI supports:

- Flood prediction.

- Drought monitoring.

- Cyclone forecasting.

- Early warning systems.

These applications strengthen disaster preparedness and resilience.

Benefits of AI in Governance

Properly implemented, AI offers several advantages.

Faster Decision-Making

AI rapidly analyses large datasets that would otherwise require extensive manual effort.

Improved Accuracy

Automated analysis reduces computational errors and improves consistency.

Greater Transparency

Digital systems generate audit trails that strengthen accountability.

Predictive Governance

AI enables governments to anticipate problems before they become crises.

Better Resource Utilisation

Public resources can be allocated more efficiently using evidence-based analysis.

Improved Citizen Services

Automation reduces delays while improving accessibility and responsiveness.

Challenges of AI in Governance

Despite its potential, AI also raises important governance challenges.

Data Privacy

AI systems require large volumes of data. Protecting citizens’ personal information is therefore essential.

Algorithmic Bias

AI systems may unintentionally reproduce biases present in training data. This may affect fairness in public decision-making.

Cybersecurity

Digital governance platforms become attractive targets for cyberattacks. Robust cybersecurity measures are therefore indispensable.

Capacity Building

Public officials require specialised training to effectively manage AI-enabled systems.

Ethical Concerns

AI should support human decision-making rather than replace administrative accountability. Government decisions affecting citizens must remain transparent, explainable, and subject to oversight.

Public Financial Management

Every government collects public resources through taxes, borrowing, non-tax revenue, and other sources. These resources must then be allocated, spent, monitored, and evaluated in accordance with constitutional principles and legislative authorisation. This entire process is known as Public Financial Management (PFM).

PFM encompasses:

- Budget preparation.

- Budget execution.

- Public expenditure.

- Financial reporting.

- Accounting.

- Auditing.

- Internal financial controls.

- Performance evaluation.

An effective PFM system ensures that public money is spent economically, efficiently, effectively, and for its intended purposes. The Rural Internal Audit Portal strengthens one of the most important components of PFM—internal auditing.

Why Public Financial Management Matters

Strong public financial management contributes to:

- Fiscal discipline.

- Efficient utilisation of public resources.

- Improved service delivery.

- Better development outcomes.

- Reduced corruption.

- Increased investor confidence.

- Higher public trust in government institutions.

Conversely, weak financial management may result in:

- Wasteful expenditure.

- Leakages.

- Fraud.

- Delays.

- Poor programme implementation.

- Reduced accountability.

Thus, sound financial management forms the backbone of good governance.

Internal Financial Controls, Internal Auditing, and the Foundations of Accountable Governance

No government, regardless of its administrative capacity or technological sophistication, can achieve good governance without robust systems for monitoring how public money is collected, managed, and spent. Every year, governments allocate enormous financial resources to sectors such as education, healthcare, rural development, infrastructure, agriculture, social protection, and environmental conservation. These public funds are entrusted to thousands of ministries, departments, public sector undertakings, autonomous bodies, local governments, and implementing agencies.

The success of public policy depends not only on the amount of money allocated but also on whether it is utilised efficiently, legally, transparently, and for the intended purpose. Even well-designed welfare schemes can fail if funds are mismanaged, diverted, delayed, or spent without achieving the desired outcomes.

Traditionally, governments relied heavily on post-facto inspections and external audits to identify irregularities. While these mechanisms remain essential, they often detect problems only after financial losses have already occurred. Modern public administration therefore places increasing emphasis on preventive governance, where risks are identified early and corrective action is taken before serious irregularities emerge.

This preventive approach is made possible through Internal Financial Controls (IFCs) and Internal Auditing, which together form the first line of defence against financial mismanagement, inefficiency, fraud, and weak programme implementation.

The AI-enabled Rural Internal Audit Portal reflects this shift towards continuous, technology-driven oversight. Rather than waiting for annual reviews, the portal seeks to identify risks proactively, strengthen internal controls, and support evidence-based decision-making across rural development programmes.

Internal Financial Controls (IFCs)

Before understanding internal audits, it is important to understand Internal Financial Controls (IFCs). Internal Financial Controls are the policies, procedures, organisational structures, and administrative mechanisms established within an organisation to ensure that financial resources are managed responsibly and organisational objectives are achieved.

They are designed to provide reasonable assurance that:

- Public money is used only for authorised purposes.

- Financial transactions are accurately recorded.

- Assets are safeguarded against loss or misuse.

- Laws, rules, and regulations are followed.

- Fraud and errors are prevented or detected promptly.

- Operational efficiency is continuously improved.

Unlike audits, which periodically examine organisational performance, internal financial controls operate every day as part of routine administration.

Objectives of Internal Financial Controls

A robust system of internal financial controls seeks to achieve several important objectives.

1. Safeguarding Public Resources

Governments manage enormous public assets, including financial resources, infrastructure, equipment, records, and public property. Internal controls help prevent:

- Theft.

- Misappropriation.

- Unauthorised expenditure.

- Damage to public assets.

- Financial leakages.

2. Ensuring Financial Accuracy

Reliable financial information is essential for effective decision-making. Internal controls promote:

- Accurate accounting.

- Proper documentation.

- Timely financial reporting.

- Reliable financial statements.

Decision-makers can therefore allocate resources more effectively.

3. Ensuring Legal Compliance

Government departments operate within an extensive legal framework. Internal controls ensure compliance with:

- Financial Rules.

- Budget provisions.

- Procurement procedures.

- Service rules.

- Departmental guidelines.

- Statutory regulations.

This reduces the risk of administrative irregularities.

4. Improving Operational Efficiency

Effective controls eliminate unnecessary delays, duplication of work, and inefficient administrative practices. Improved efficiency ultimately benefits both government institutions and citizens.

5. Strengthening Public Trust

Transparent financial management enhances public confidence in government institutions. Citizens are more likely to trust public programmes when resources are managed responsibly.

Components of Internal Financial Controls

An effective internal control system consists of several interconnected elements.

Control Environment

The control environment refers to the organisational culture that promotes ethical behaviour, accountability, integrity, and responsible financial management. Leadership commitment plays a decisive role in creating this environment.

Risk Assessment

Government departments must continuously identify risks that could affect programme implementation. These risks may include:

- Financial fraud.

- Procurement irregularities.

- Weak documentation.

- Delayed fund utilisation.

- Technological failures.

- Cybersecurity threats.

Understanding these risks enables administrators to design appropriate control mechanisms.

Control Activities

Control activities are the specific procedures implemented to minimise identified risks. Examples include:

- Approval hierarchies.

- Segregation of duties.

- Budgetary controls.

- Procurement checks.

- Financial authorisations.

- Digital verification systems.

Information and Communication

Reliable information must flow efficiently across the organisation. Timely reporting enables managers to identify emerging issues and take corrective action.

Monitoring

Internal controls require continuous monitoring to ensure that they remain effective over time. Monitoring may involve:

- Internal audits.

- Supervisory reviews.

- Performance assessments.

- Digital dashboards.

- Compliance reports.

Why Governments Need Internal Audits

Even the strongest internal control system cannot eliminate every risk. Unexpected circumstances, human error, technological failures, changing regulations, and evolving fraud techniques require continuous independent evaluation. This is the role of Internal Audit.

Internal auditing is a systematic, independent, and objective process that evaluates whether an organisation’s governance, risk management, and internal control systems are functioning effectively. Unlike external audits conducted after financial statements are prepared, internal audits operate continuously throughout the year.

They help organisations identify weaknesses before they become major administrative failures.

Objectives of Internal Auditing

Internal auditing supports organisational improvement rather than merely identifying mistakes. Its major objectives include:

- Evaluating internal controls.

- Assessing compliance with rules and regulations.

- Identifying operational risks.

- Improving efficiency.

- Detecting financial irregularities.

- Strengthening governance.

- Supporting informed decision-making.

Thus, internal audit functions as an advisory as well as an assurance mechanism.

Evolution of Internal Auditing

Historically, auditing focused primarily on verifying financial transactions and detecting fraud. Over time, the scope of internal auditing expanded significantly.

Traditional Internal Audit

Earlier audits primarily examined:

- Accounting records.

- Vouchers.

- Receipts.

- Financial statements.

- Cash balances.

The emphasis was on financial accuracy.

Modern Internal Audit

Contemporary internal auditing adopts a much broader perspective. It evaluates:

- Governance.

- Risk management.

- Internal controls.

- Programme implementation.

- Operational efficiency.

- Information systems.

- Organisational performance.

Thus, internal audit has evolved from a narrow accounting exercise into a strategic governance function.

Difference Between Audit, Inspection, Vigilance, Investigation, and Social Audit

One of the most common areas of confusion in public administration is the distinction among these mechanisms. Although all seek to improve accountability, they differ significantly in purpose and methodology.

| Mechanism | Primary Objective | Conducted By | Nature |

|---|---|---|---|

| Audit | Evaluates financial management, compliance, efficiency, and internal controls | Internal auditors or external audit institutions | Independent and systematic |

| Inspection | Examines day-to-day functioning and implementation | Supervisory officers | Administrative review |

| Vigilance | Prevents and detects corruption and misconduct | Vigilance organisations | Preventive and disciplinary |

| Investigation | Determines facts relating to specific allegations or offences | Investigative agencies | Fact-finding and evidence collection |

| Social Audit | Enables citizens to verify programme implementation | Community members, Gram Sabhas, civil society | Participatory accountability |

Understanding these differences is essential because each mechanism complements the others rather than replacing them.

Internal Audit vs External Audit

Another important distinction is between internal and external auditing.

| Internal Audit | External Audit |

|---|---|

| Conducted by the organisation or an independent internal audit unit. | Conducted by an independent external authority such as the Comptroller and Auditor General (CAG) in the public sector. |

| Continuous throughout the year. | Periodic, usually after the completion of financial activities. |

| Focuses on improving governance, risk management, and internal controls. | Focuses on providing independent assurance regarding financial statements, legality, and performance. |

| Primarily serves management. | Primarily serves Parliament, legislatures, and the public. |

| Advisory as well as assurance-oriented. | Independent assurance and accountability-oriented. |

Both are essential components of a robust public financial management system.

Why AI is Transforming Internal Auditing

Traditional internal audits relied heavily on manual document verification, sample-based testing, and periodic field visits. While effective, these approaches had limitations in terms of speed, scalability, and real-time risk detection.

Artificial Intelligence is fundamentally transforming this process.

AI-enabled audit systems can:

- Analyse millions of transactions within seconds.

- Detect unusual expenditure patterns.

- Identify duplicate payments.

- Highlight procurement anomalies.

- Generate risk scores for projects.

- Prioritise high-risk cases for detailed examination.

- Produce automated dashboards and reports.

Instead of reviewing only a sample of transactions, AI enables auditors to analyse entire datasets, improving both the efficiency and accuracy of audits. This shift from reactive auditing to predictive and risk-based auditing represents one of the most significant reforms in modern public financial management.

The Rural Internal Audit Portal is an important example of this transformation. By integrating AI with internal auditing, the Ministry of Rural Development aims to strengthen financial oversight, improve compliance, identify risks proactively, and enhance transparency across rural development programmes.

Understanding Auditing – Meaning, Evolution, Principles, and Objectives

Every organised institution—whether a government ministry, private company, university, non-governmental organisation, cooperative society, or international organisation—manages resources entrusted to it by stakeholders. Governments manage taxpayers’ money, companies manage shareholders’ investments, banks manage depositors’ savings, and charitable organisations administer public donations. In each case, those who provide resources expect them to be used honestly, efficiently, and for the intended purpose.

This expectation creates a fundamental governance question: How can stakeholders be assured that resources are being managed responsibly? The answer lies in auditing.

Auditing is one of the oldest and most important mechanisms for ensuring accountability. It provides an independent assessment of whether financial transactions, administrative processes, and organisational activities conform to applicable laws, policies, standards, and objectives.

Although auditing is often associated with checking accounts or detecting fraud, its contemporary role extends much further. Modern auditing evaluates governance systems, risk management practices, operational efficiency, programme implementation, internal controls, information systems, environmental performance, and achievement of organisational objectives.

Consequently, auditing has evolved from a bookkeeping exercise into a strategic instrument of good governance.

What is an Audit?

An audit is a systematic, independent, objective, and evidence-based examination of an organisation’s financial records, operations, processes, systems, or programmes to determine whether they comply with established criteria and whether organisational objectives are being achieved efficiently, effectively, economically, and ethically.

Several features distinguish auditing from routine administrative supervision. First, auditing is systematic. It follows a structured methodology rather than relying on ad hoc observations. Second, auditing is independent. Auditors must maintain objectivity and avoid conflicts of interest. Third, auditing is evidence-based. Findings are supported by verifiable documents, records, interviews, physical observations, and analytical procedures rather than assumptions.

Finally, auditing aims not merely to identify deficiencies but also to recommend improvements that strengthen governance and organisational performance.

Key Characteristics of Auditing

An effective audit possesses several defining characteristics.

Independence

Auditors must remain free from undue influence by the management whose activities they examine. Independence ensures credibility and public confidence in audit findings.

Objectivity

Audit conclusions should be based exclusively on evidence rather than personal opinions, political considerations, or institutional bias. Objectivity enhances fairness and reliability.

Systematic Process

Auditing follows a structured sequence involving:

- Planning.

- Risk assessment.

- Evidence collection.

- Analysis.

- Reporting.

- Follow-up.

This methodology promotes consistency across different audit assignments.

Evidence-Based Assessment

Reliable audit conclusions require sufficient and appropriate evidence. Auditors therefore examine:

- Financial documents.

- Administrative records.

- Contracts.

- Procurement files.

- Digital databases.

- Physical assets.

- Interviews.

- Field observations.

Evidence strengthens the validity of audit recommendations.

Improvement-Oriented

Modern auditing seeks to improve governance rather than merely identify mistakes. Its recommendations help organisations strengthen internal controls, reduce risks, improve efficiency, and enhance accountability.

Evolution of Auditing

The history of auditing closely parallels the evolution of organised administration.

Ancient Civilisations

Evidence of auditing practices can be traced to ancient Egypt, Mesopotamia, Greece, Rome, and India. Ancient rulers appointed officials to verify tax collections, monitor public expenditure, and prevent misuse of state resources. In ancient India, texts such as the Arthashastra emphasised meticulous record-keeping, financial accountability, and regular inspection of state officials.

Kautilya recognised that officials entrusted with public money required continuous supervision because opportunities for financial irregularities inevitably arise wherever public resources are managed. This observation remains remarkably relevant in contemporary public administration.

Medieval Period

As kingdoms expanded, specialised officials increasingly supervised revenue collection and expenditure. Auditing remained primarily focused on verifying financial accounts and detecting fraud.

Industrial Revolution

The Industrial Revolution transformed auditing fundamentally. Large corporations emerged with thousands of shareholders who were separated from day-to-day management. This separation created an agency problem.

Owners required independent verification that managers were using company resources responsibly. Consequently, professional auditing expanded rapidly.

Twentieth Century

During the twentieth century, governments assumed much broader developmental responsibilities. Public expenditure increased dramatically in sectors such as:

- Education.

- Health.

- Agriculture.

- Infrastructure.

- Social welfare.

Auditing therefore expanded beyond financial verification to include programme implementation and performance assessment.

Twenty-First Century

Modern auditing incorporates:

- Risk management.

- Governance evaluation.

- Information technology.

- Environmental sustainability.

- Cybersecurity.

- Artificial Intelligence.

- Data analytics.

- Performance auditing.

Auditors increasingly function as strategic advisors supporting organisational improvement rather than merely financial inspectors.

Why Auditing is Necessary

Every organisation faces uncertainty. Resources may be misused intentionally through fraud or unintentionally through administrative inefficiency, weak controls, inadequate training, or poor decision-making. Auditing provides assurance that these risks are appropriately managed. Its importance extends across multiple dimensions.

Promoting Accountability

Auditing ensures that officials entrusted with public resources remain answerable for their decisions. Accountability strengthens democratic governance by reinforcing public trust.

Preventing Fraud and Corruption

Although auditing cannot eliminate corruption completely, strong audit systems significantly increase the likelihood that irregularities will be detected. This deterrent effect discourages financial misconduct.

Improving Financial Management

Auditing evaluates whether financial resources are utilised:

- Economically.

- Efficiently.

- Effectively.

Better financial management ultimately improves development outcomes.

Ensuring Legal Compliance

Government departments must comply with numerous laws, regulations, financial rules, procurement guidelines, and administrative procedures. Auditing verifies adherence to these legal requirements.

Supporting Better Decision-Making

Audit findings provide valuable information regarding organisational strengths, weaknesses, risks, and opportunities for improvement. Management can therefore make more informed decisions.

Enhancing Public Confidence

Transparent audit processes strengthen citizens’ confidence in public institutions. Trust is particularly important for governments managing large welfare programmes funded by taxpayers.

Objectives of Auditing

Although different organisations conduct audits for different purposes, most audits pursue several common objectives.

Verify Accuracy

Auditors verify whether financial records accurately reflect organisational transactions. Reliable accounting forms the basis of sound decision-making.

Assess Compliance

Audits examine whether organisational activities comply with:

- Laws.

- Financial rules.

- Procurement regulations.

- Government guidelines.

- Internal policies.

Compliance reduces legal and administrative risks.

Evaluate Internal Controls

Auditors assess whether existing internal control systems effectively prevent errors, fraud, and inefficiency. Weak controls are often identified before significant losses occur.

Improve Operational Efficiency

Modern auditing examines whether organisational resources are being utilised optimally. Recommendations frequently focus on:

- Reducing delays.

- Eliminating duplication.

- Improving workflow.

- Enhancing productivity.

Support Risk Management

Auditors identify emerging risks that may threaten organisational objectives. Management can then implement preventive measures before risks materialise.

Promote Good Governance

Ultimately, auditing strengthens:

- Transparency.

- Accountability.

- Integrity.

- Ethical conduct.

- Public trust.

Thus, auditing serves as an essential pillar of democratic governance.

Fundamental Principles of Auditing

Professional auditing is guided by universally recognised principles.

Integrity

Auditors must demonstrate honesty, fairness, and ethical conduct throughout the audit process. Integrity forms the foundation of professional credibility.

Independence

Auditors should remain free from external pressure or conflicts of interest. Independent audits generate greater public confidence.

Professional Competence

Auditors require specialised knowledge in:

- Accounting.

- Finance.

- Law.

- Public administration.

- Information systems.

- Risk management.

Continuous professional development is therefore essential.

Confidentiality

Auditors frequently access sensitive organisational information. They must protect confidential data while using it solely for legitimate audit purposes.

Due Professional Care

Audit work should be performed diligently using appropriate methodologies and sufficient evidence. Carelessness may compromise audit quality.

Evidence-Based Conclusions

Audit findings should always be supported by reliable, relevant, and sufficient evidence. Unsupported allegations undermine the credibility of the audit process.

Auditing in Democratic Governance

In democratic societies, auditing serves purposes extending far beyond financial management. It strengthens constitutional governance by ensuring that executive authorities remain accountable for their use of public resources.

Auditing therefore contributes directly to:

- Fiscal responsibility.

- Rule of law.

- Transparency.

- Accountability.

- Responsible public expenditure.

- Effective implementation of welfare schemes.

Institutions such as internal audit units, finance departments, legislative committees, and supreme audit institutions collectively reinforce democratic accountability.

As governments increasingly adopt digital platforms and artificial intelligence, auditing itself is undergoing profound transformation. Rather than relying solely on retrospective examination, modern audit systems increasingly support continuous assurance, predictive analytics, and real-time risk identification.

The AI-enabled Rural Internal Audit Portal represents one such innovation, demonstrating how technology can strengthen governance by making internal auditing faster, smarter, and more preventive.

Types of Audits

Auditing is not a single, uniform activity. Different organisations face different objectives, risks, legal obligations, and operational challenges. Consequently, no single audit can evaluate every aspect of an organisation’s functioning.

For example, verifying whether expenditure has been recorded correctly requires a different approach from assessing whether a welfare programme has improved the lives of beneficiaries. Similarly, examining compliance with procurement rules differs from investigating suspected financial fraud or evaluating the security of an information technology system.

Over time, the discipline of auditing has therefore evolved into several specialised branches, each designed to address a distinct aspect of organisational governance.

Collectively, these audits strengthen transparency, accountability, efficiency, and public trust by ensuring that organisations not only spend resources lawfully but also achieve intended outcomes.

The AI-enabled Rural Internal Audit Portal integrates several of these approaches—particularly internal auditing, compliance auditing, and risk-based auditing—into a unified digital platform.

Classification of Audits

Audits may be classified on the basis of their purpose, scope, timing, methodology, or institutional responsibility.

The major categories include:

- Financial Audit

- Compliance Audit

- Performance Audit

- Operational Audit

- Internal Audit

- External Audit

- Forensic Audit

- Information Systems (IT) Audit

- Environmental Audit

- Risk-Based Audit

- Continuous Audit

Each type complements the others rather than replacing them.

Financial Audit

A Financial Audit examines whether an organisation’s financial statements accurately present its financial position in accordance with applicable accounting standards and legal requirements.

It is the most traditional and widely recognised form of auditing. The primary objective is to provide assurance that financial records are free from material misstatements caused by fraud or error.

Objectives

Financial audits seek to:

- Verify the accuracy of financial statements.

- Ensure proper accounting of income and expenditure.

- Confirm existence of assets and liabilities.

- Detect accounting errors.

- Strengthen financial credibility.

Importance

Reliable financial information enables:

- Better decision-making.

- Investor confidence.

- Public accountability.

- Effective financial management.

In the public sector, financial audits reassure taxpayers that government accounts accurately reflect public expenditure.

Compliance Audit

A Compliance Audit examines whether organisational activities comply with applicable:

- Laws.

- Rules.

- Regulations.

- Government guidelines.

- Administrative procedures.

- Contractual obligations.

Rather than asking whether expenditure was accurately recorded, compliance audits ask whether the expenditure was authorised and legally permissible.

Objectives

Compliance audits verify:

- Adherence to financial rules.

- Procurement procedures.

- Budget provisions.

- Service regulations.

- Statutory requirements.

Example

Suppose a government department purchases medical equipment.

A compliance audit would examine whether:

- Proper procurement procedures were followed.

- Competitive bidding requirements were satisfied.

- Financial approvals were obtained.

- Expenditure remained within budgetary limits.

Importance

Compliance auditing promotes:

- Rule of law.

- Administrative discipline.

- Prevention of irregular expenditure.

- Institutional accountability.

The Rural Internal Audit Portal places significant emphasis on compliance auditing.

Performance Audit

A Performance Audit evaluates whether government programmes achieve their intended objectives while utilising resources economically, efficiently, and effectively. Unlike financial audits, performance audits focus primarily on results rather than accounts.

Example

In the case of a rural housing scheme, performance auditors may examine:

- Number of houses completed.

- Construction quality.

- Timeliness.

- Beneficiary satisfaction.

- Achievement of programme objectives.

Importance

Performance auditing strengthens:

- Public policy evaluation.

- Outcome-based governance.

- Efficient utilisation of public resources.

It has become increasingly important as governments shift towards results-oriented administration.

Operational Audit

An Operational Audit evaluates organisational processes, systems, and procedures to identify opportunities for improving efficiency and productivity.

Operational audits focus primarily on how work is performed.

Objectives

Operational audits seek to:

- Reduce administrative delays.

- Improve workflow.

- Eliminate duplication.

- Strengthen internal coordination.

- Improve service delivery.

Example

An operational audit of a district office may examine:

- File movement.

- Approval timelines.

- Staff deployment.

- Digital workflows.

- Resource utilisation.

Importance

Operational auditing supports administrative reforms by improving organisational effectiveness.

Internal Audit

An Internal Audit is an independent, objective assurance and advisory activity conducted within an organisation to improve governance, risk management, and internal control systems.

Unlike external audits, internal audits function continuously throughout the year.

Objectives

Internal audits seek to:

- Evaluate governance systems.

- Assess internal controls.

- Identify operational risks.

- Improve organisational performance.

- Strengthen accountability.

Characteristics

Internal audits are:

- Continuous.

- Preventive.

- Improvement-oriented.

- Advisory.

- Risk-focused.

Importance

Modern organisations increasingly rely upon internal audits as a strategic management tool rather than merely a compliance mechanism.

The Rural Internal Audit Portal primarily supports this type of auditing.

External Audit

An External Audit is conducted by an independent authority outside the organisation.

In India, the Comptroller and Auditor General (CAG) performs external audits of government accounts and public sector entities in accordance with constitutional provisions.

Objectives

External audits provide independent assurance regarding:

- Financial statements.

- Compliance.

- Performance.

- Accountability.

Importance

External auditing strengthens legislative oversight because audit reports are examined by Parliament and State Legislatures through committees such as the Public Accounts Committee (PAC).

Forensic Audit

A Forensic Audit is a specialised investigation undertaken when fraud, corruption, embezzlement, or financial misconduct is suspected.

Unlike routine audits, forensic audits collect evidence that may be used in judicial proceedings.

Objectives

Forensic audits seek to:

- Identify fraudulent transactions.

- Trace financial irregularities.

- Collect admissible evidence.

- Support criminal investigations.

Importance

Forensic auditing plays an increasingly important role in combating financial crimes and strengthening anti-corruption efforts.

Information Systems (IT) Audit

An Information Systems Audit evaluates whether information technology systems adequately protect organisational data while supporting operational objectives.

As governments increasingly digitise their services, IT auditing has become essential.

Areas Covered

IT audits examine:

- Cybersecurity.

- Data integrity.

- System availability.

- Access controls.

- Disaster recovery.

- Software reliability.

Importance

Digital governance cannot succeed without secure and reliable information systems.

Environmental Audit

An Environmental Audit evaluates whether organisational activities comply with environmental laws and sustainable development objectives.

Objectives

Environmental audits assess:

- Pollution control.

- Waste management.

- Resource efficiency.

- Environmental compliance.

- Climate sustainability.

Importance

Growing global concern regarding climate change has increased the significance of environmental auditing in both public and private sectors.

Risk-Based Audit

Traditional auditing allocated similar attention to all organisational activities regardless of their relative importance.

Modern auditing adopts a different philosophy.

A Risk-Based Audit (RBA) focuses audit resources on areas presenting the greatest risk to organisational objectives.

Rather than auditing everything equally, auditors identify high-risk activities and prioritise them for detailed examination.

Risk Assessment

Risk-based auditing begins by identifying potential threats such as:

- Financial irregularities.

- Procurement risks.

- Weak internal controls.

- Delayed programme implementation.

- Cybersecurity vulnerabilities.

- High-value contracts.

Each risk is evaluated according to:

- Probability of occurrence.

- Potential impact.

Benefits

Risk-based auditing:

- Improves audit efficiency.

- Optimises resource allocation.

- Detects emerging problems earlier.

- Supports preventive governance.

The Rural Internal Audit Portal incorporates AI to strengthen precisely this type of auditing.

Continuous Audit

Traditional audits were conducted annually or periodically.

Continuous auditing represents a significant evolution.

Using digital technologies, continuous audits monitor transactions almost in real time rather than waiting until the end of the financial year.

Advantages

Continuous auditing enables:

- Early detection of irregularities.

- Faster corrective action.

- Real-time monitoring.

- Improved compliance.

- Better governance.

Artificial Intelligence significantly enhances continuous auditing by analysing large datasets automatically.

Comparative Overview of Major Audit Types

| Audit Type | Primary Focus | Key Question |

|---|---|---|

| Financial Audit | Financial statements | Are the accounts accurate? |

| Compliance Audit | Laws and rules | Were procedures followed? |

| Performance Audit | Outcomes | Were objectives achieved economically, efficiently, and effectively? |

| Operational Audit | Administrative processes | Can organisational efficiency be improved? |

| Internal Audit | Governance, controls, risks | Are internal systems functioning effectively? |

| External Audit | Independent assurance | Is the organisation accountable to stakeholders? |

| Forensic Audit | Fraud investigation | Has financial misconduct occurred? |

| IT Audit | Information systems | Are digital systems secure and reliable? |

| Environmental Audit | Environmental performance | Are sustainability obligations being fulfilled? |

| Risk-Based Audit | High-risk activities | Where should audit attention be concentrated? |

| Continuous Audit | Real-time monitoring | Can problems be identified before they escalate? |

Why These Audit Types Matter for the Rural Internal Audit Portal

The AI-enabled Rural Internal Audit Portal is not limited to one form of auditing. It brings together multiple audit concepts within a single digital ecosystem.

The portal:

- Strengthens internal audits by providing continuous oversight.

- Enhances compliance audits through automated rule-based verification.

- Supports risk-based audits using AI-driven risk identification.

- Facilitates elements of continuous auditing through digital workflows and real-time monitoring.

- Improves governance by integrating data analytics with public financial management.

This integrated approach represents a major shift from manual, periodic, and reactive audits to intelligent, technology-enabled, and preventive governance.

Risk Management and Risk-Based Auditing

Traditional auditing was largely reactive. Auditors examined records after transactions had been completed and programmes had been implemented. Although such audits remain essential, they often identify irregularities only after financial losses have occurred, resources have been wasted, or programme objectives have already been compromised.

Modern governance increasingly demands a different approach—one that identifies risks before they materialise and enables administrators to take preventive action. This philosophy has given rise to Risk-Based Auditing (RBA).

Instead of allocating equal audit attention to every office, programme, or transaction, Risk-Based Auditing prioritises areas where the likelihood and consequences of failure are greatest. In doing so, it enables governments to use limited audit resources more effectively while strengthening transparency, accountability, and programme performance.

The AI-enabled Rural Internal Audit Portal operationalises this philosophy by integrating artificial intelligence with audit planning, allowing the Ministry of Rural Development to identify high-risk programmes and institutions for focused internal audits.

Understanding Risk

Before studying Risk-Based Auditing, it is necessary to understand the concept of risk. A risk is the possibility that an event or circumstance may prevent an organisation from achieving its objectives. Risk does not necessarily imply that something undesirable will definitely occur. Rather, it reflects uncertainty regarding future events and their potential impact on organisational performance.

Every organisation—whether public or private—faces risks because future conditions are never completely predictable.

Risk in Public Administration

Government programmes operate in complex environments involving multiple stakeholders, diverse geographical conditions, evolving regulations, and significant financial resources. Consequently, public institutions face numerous risks.

Examples include:

- Financial mismanagement.

- Procurement irregularities.

- Delays in project implementation.

- Cost overruns.

- Weak documentation.

- Information technology failures.

- Cybersecurity incidents.

- Natural disasters.

- Human resource shortages.

- Policy changes.

These risks may reduce programme effectiveness, increase costs, or undermine public trust.

Characteristics of Risk

Several characteristics define organisational risk.

Uncertainty

Risk relates to uncertain future events rather than known outcomes.

Probability

Every risk has a likelihood of occurring. Some risks are highly probable, whereas others occur rarely.

Impact

Different risks produce different consequences. Some may cause minor administrative inconvenience, while others may result in major financial losses or programme failure.

Dynamic Nature

Risks continuously evolve because of changing technologies, economic conditions, laws, and organisational structures. Risk management must therefore remain an ongoing process.

Categories of Risk in Government

Public administration involves multiple categories of risk.

Financial Risk

Financial risks arise from:

- Fraud.

- Misappropriation.

- Budget overruns.

- Unauthorised expenditure.

- Weak accounting systems.

Operational Risk

Operational risks result from failures in organisational processes. Examples include:

- Delayed approvals.

- Inefficient workflows.

- Human error.

- Equipment failure.

Compliance Risk

Government organisations must comply with numerous legal and regulatory requirements. Failure to comply may result in:

- Legal disputes.

- Administrative action.

- Financial penalties.

- Loss of credibility.

Strategic Risk

Strategic risks affect an organisation’s ability to achieve its long-term objectives. Examples include:

- Poor policy design.

- Inadequate planning.

- Demographic changes.

- Climate-related challenges.

Reputational Risk

Public confidence may decline because of:

- Corruption.

- Poor service delivery.

- Data breaches.

- Administrative failures.

Reputational damage often affects organisational effectiveness even when financial losses are limited.

Technological Risk

Increasing digitalisation exposes governments to risks relating to:

- Cybersecurity.

- System failures.

- Data corruption.

- Artificial Intelligence errors.

- Software vulnerabilities.

What is Risk Management?

Risk management is the systematic process of identifying, analysing, evaluating, mitigating, monitoring, and reviewing risks that may affect organisational objectives.

Contrary to popular belief, risk management does not seek to eliminate all risks. Such an objective would be impossible because every organisation operates under conditions of uncertainty.

Instead, risk management seeks to:

- Understand risks.

- Prioritise them.

- Reduce unacceptable risks.

- Prepare contingency measures.

- Improve organisational resilience.

Thus, risk management supports informed decision-making rather than risk avoidance.

Objectives of Risk Management

Effective risk management seeks to:

- Protect public resources.

- Improve programme implementation.

- Strengthen governance.

- Enhance organisational resilience.

- Improve public confidence.

- Support better policymaking.

- Facilitate informed decision-making.

Risk Management Process

Risk management follows a structured sequence of activities.

Step 1: Risk Identification

The first step involves identifying events that could affect organisational objectives.

Information may be obtained from:

- Previous audit reports.

- Financial statements.

- Field inspections.

- Stakeholder consultations.

- Data analytics.

- Citizen grievances.

- Management reviews.

Step 2: Risk Assessment

Identified risks are evaluated according to two principal criteria.

Probability

How likely is the risk to occur?

Impact

If the risk occurs, how severe will its consequences be?

Risks combining high probability with high impact receive the highest priority.

Step 3: Risk Prioritisation

Since organisational resources are limited, all risks cannot receive equal attention.

Risks are therefore prioritised according to:

- Severity.

- Urgency.

- Organisational significance.

This prioritisation forms the foundation of Risk-Based Auditing.

Step 4: Risk Mitigation

Appropriate measures are implemented to reduce identified risks.

Examples include:

- Strengthening internal controls.

- Staff training.

- Policy revisions.

- Technology upgrades.

- Enhanced supervision.

Step 5: Continuous Monitoring

Risk management is not a one-time activity.

Organisations continuously monitor risk indicators because circumstances evolve over time.

Digital dashboards and AI-powered analytics increasingly support continuous monitoring.

Risk Matrix

A Risk Matrix is a tool used to classify risks based on their probability and impact.

| Probability | Low Impact | Medium Impact | High Impact |

|---|---|---|---|

| Low | Low Risk | Low–Medium Risk | Medium Risk |

| Medium | Low–Medium Risk | Medium Risk | High Risk |

| High | Medium Risk | High Risk | Very High Risk |

Risks classified as Very High Risk generally receive immediate management attention and are prioritised during audit planning.

What is Risk-Based Auditing (RBA)?

Risk-Based Auditing is an audit methodology that allocates audit resources according to the level of risk faced by different organisational activities.

Rather than auditing every programme with identical intensity, RBA focuses on those areas where failures would have the greatest likelihood or consequences.

In simple terms:

Traditional Audit asks: What should we audit?

Risk-Based Audit asks: Where are the greatest risks to achieving organisational objectives?

This shift makes auditing more efficient, strategic, and preventive.

Evolution of Risk-Based Auditing

Traditional audit systems often followed fixed schedules or rotational cycles.

Every office or programme received similar audit attention irrespective of:

- Financial size.

- Operational complexity.

- Historical performance.

- Risk exposure.

Modern governance recognises that this approach may not optimise limited audit resources.

Consequently, Risk-Based Auditing has emerged as an internationally accepted best practice.

Today, governments, supreme audit institutions, multilateral organisations, and private enterprises increasingly adopt RBA to improve audit effectiveness.

Principles of Risk-Based Auditing

Risk-Based Auditing is guided by several core principles.

Focus on Organisational Objectives

Audit planning begins with organisational objectives rather than accounting records alone.

Prioritisation of High-Risk Areas

Limited audit resources should focus on activities posing the greatest threats.

Dynamic Planning

Audit plans should evolve as organisational risks change.

Continuous Risk Assessment

Risk identification continues throughout the audit cycle.

Evidence-Based Decisions

Risk assessments should rely upon objective evidence rather than assumptions.

Advantages of Risk-Based Auditing

Risk-Based Auditing offers numerous benefits.

Better Resource Allocation

Audit resources concentrate on areas where they generate maximum value.

Early Detection

Potential problems are identified before they become major administrative failures.

Improved Governance

Management receives timely information regarding emerging risks.

Enhanced Accountability

High-risk programmes receive greater scrutiny, strengthening financial discipline.

Better Decision-Making

Evidence-based risk analysis improves managerial decisions.

Stronger Public Trust

Preventing failures is generally more effective than correcting them after they occur.

Challenges of Risk-Based Auditing

Despite its advantages, RBA also faces challenges.

- Reliable data may not always be available.

- Risk assessment requires specialised expertise.

- Organisational risks change continuously.

- AI models may generate false positives or overlook emerging risks.

- Capacity building is essential for successful implementation.

These challenges highlight the importance of combining technology with human professional judgment.

Artificial Intelligence and Risk-Based Auditing

Artificial Intelligence has transformed Risk-Based Auditing by enabling continuous analysis of vast datasets.

Instead of relying primarily on manual sampling, AI systems can:

- Analyse millions of transactions simultaneously.

- Detect unusual expenditure patterns.

- Identify duplicate or suspicious payments.

- Generate automated risk scores.

- Predict emerging financial risks.

- Recommend audit priorities.

- Produce real-time dashboards.

This significantly improves the efficiency, coverage, and timeliness of internal audits.

Why Risk-Based Auditing Matters for Rural Development

The Ministry of Rural Development implements some of India’s largest public expenditure programmes, including rural housing, rural roads, livelihoods, wage employment, and social protection initiatives. These programmes involve:

- Thousands of implementing agencies.

- Millions of beneficiaries.

- Large financial outlays.

- Diverse geographical conditions.

- Multiple levels of administration.

Auditing every activity with equal intensity is neither practical nor efficient.

Risk-Based Auditing enables the Ministry to identify districts, schemes, or implementing agencies with higher risk profiles and allocate audit resources accordingly. This improves oversight, strengthens internal controls, and supports better utilisation of public funds.

The AI-enabled Rural Internal Audit Portal is designed around this principle, making risk assessment a central element of internal audit planning.

Rural Internal Audit Portal – AI-Driven Internal Auditing for Transparent and Accountable Rural Governance

Current Affairs Trigger

On 28 June 2026, Union Minister for Rural Development Shri Shivraj Singh Chouhan launched the AI-enabled Rural Internal Audit Portal during the Rashtriya Gramin Vikas Sammelan held at Pusa Campus, New Delhi. The Ministry described the platform as India’s first unified digital platform for end-to-end management of internal audits, integrating compliance audits and risk-based audits within a single technology-enabled framework.

The initiative represents an important milestone in India’s transition from periodic, manual audits to continuous, intelligent, and data-driven internal auditing.

Why Was the Rural Internal Audit Portal Needed?

The Ministry of Rural Development administers some of India’s largest and most financially significant development programmes. These include initiatives relating to wage employment, rural housing, rural roads, self-employment, livelihood promotion, watershed development, and social protection.

Implementation of these programmes involves:

- The Central Government.

- State Governments.

- District administrations.

- Panchayati Raj Institutions.

- Programme implementation agencies.

- Financial institutions.

- Community organisations.

This multi-tier governance structure results in:

- Large financial flows.

- Millions of beneficiaries.

- Thousands of implementing agencies.

- Complex administrative processes.

- Extensive documentation.

- Diverse implementation conditions.

Traditionally, internal audits relied on manual documentation, periodic inspections, and sample-based verification. While these approaches served important accountability functions, they faced several limitations.

Audits were often:

- Conducted after significant delays.

- Dependent upon physical records.

- Limited by available manpower.

- Focused primarily on detecting past irregularities.

- Less capable of identifying emerging risks.

As public expenditure expanded and governance became increasingly digital, conventional audit methods became insufficient for managing the complexity of modern rural development programmes.

The Rural Internal Audit Portal was therefore conceived as a technology-driven solution capable of strengthening internal financial oversight through Artificial Intelligence, automation, and data analytics.

Vision of the Rural Internal Audit Portal

The portal reflects a broader transformation in public administration.

Its vision is not merely to digitise audit documentation but to create an integrated governance ecosystem where:

- Risks are identified proactively.

- Internal controls are continuously strengthened.

- Audit planning becomes evidence-based.

- Compliance monitoring becomes automated.

- Decision-makers receive real-time insights.

- Public resources are managed more efficiently.

Thus, the initiative represents a shift from reactive auditing to predictive governance.

Objectives of the Portal

The Rural Internal Audit Portal pursues several interrelated objectives.

1. Strengthening Transparency

Transparent governance requires that financial transactions, administrative decisions, and audit findings be documented systematically.

Digital platforms reduce information asymmetry by creating verifiable electronic records.

This strengthens institutional credibility and public trust.

2. Improving Accountability

Internal audits help ensure that programme implementing agencies remain accountable for:

- Financial management.

- Compliance with rules.

- Programme implementation.

- Achievement of objectives.

The portal provides a structured mechanism for monitoring this accountability across different administrative levels.

3. Promoting Risk-Based Auditing

Rather than allocating equal audit attention to all programmes, the portal supports prioritisation based on risk assessment. This enables audit resources to focus on high-risk activities where oversight is most needed.

4. Standardising Internal Audit Processes

Historically, audit practices often varied across implementing agencies. The portal seeks to establish:

- Uniform procedures.

- Standardised documentation.

- Common reporting formats.

- Consistent audit methodologies.

Standardisation improves comparability and audit quality.

5. Improving Audit Efficiency

Digital workflows reduce administrative burdens associated with:

- Paper documentation.

- Manual compilation.

- Repetitive reporting.

- Physical record management.

Auditors can therefore devote greater attention to analysis and problem-solving.

6. Supporting Better Decision-Making

The portal generates structured information that assists administrators in:

- Identifying implementation gaps.

- Prioritising corrective action.

- Monitoring programme performance.

- Strengthening internal controls.

Thus, auditing becomes a management tool rather than merely a compliance exercise.

Major Features of the Rural Internal Audit Portal